Islamic banking has the potential to foster greater financial intermediation and inclusion, especially among Muslim populations that may be under-served by conventional banks, and to facilitate lending in support for small and medium sized enterprises, the IMF says.

Since Shariah allows trade with people from other religions, it is important that countries adapt their regulatory, supervisory, and consumer protection frameworks to address the unique risks in Islamic finance, take further steps to develop Shariah-compliant financial markets and monetary instruments, and strengthen the international architecture for growing cross-border operations.

The similarities between “Murabahah” and factoring that make factoring an acceptable instrument under Shariah law are :

- Order based approval where an order or sales contract is approved by the factor as per Article 17 of the GRIF.

- The factor is the sole owner of the receivable and all rights of the supplier is transferred to the factor as per Article 12 of the GRIF.

- The factor has an obligation to pay the purchase price of the receivable to the supplier on any agreed date as per Article 23 and 24 of the GRIF.

- The receivable is related to a bona fide sale of goods or rendered service as per Article 28 of the GRIF.

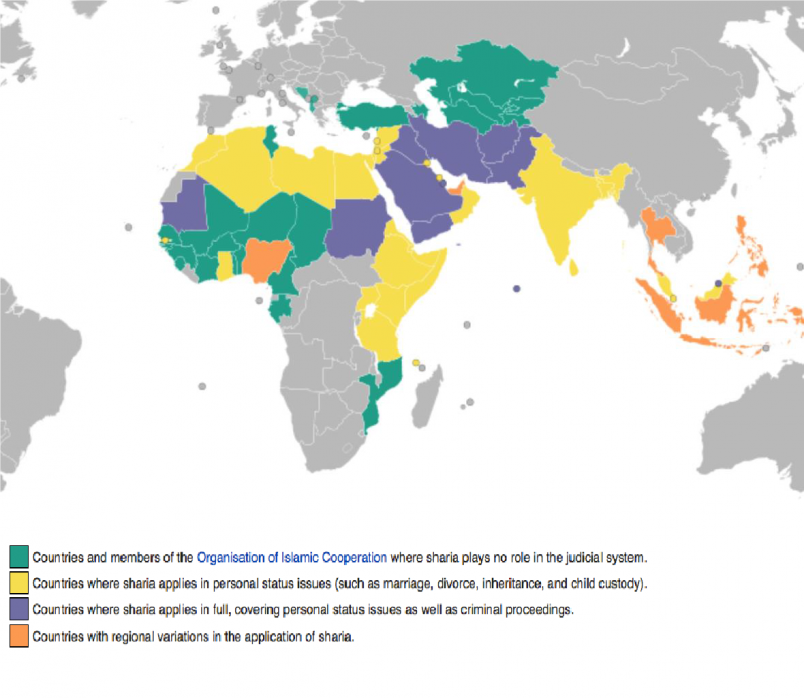

The main principles of Islamic finance are:

- Interest (riba) is prohibited in all financial transactions

- Extreme uncertainty (gharar) is prohibited on the subject contract of the transactions

- Traded goods, services and activities must be acceptable (halal) to Shariah principals and unlawful (haram) earnings and expenditures are prohibited

- The obligations of trust (amanah) and covenants (uqud) must be adhered to, while fraud of giving less than due in measure and weight and unjust enrichment are prohibited (good faith in contracting).

As can be seen, there are actually only a few differences between the General Rules for International Factoring (GRIF) and Islamic finance principles.

Consequently, the Supplemental Agreement for Islamic International Factoring has only three important deviations from the GRIF:

- As interest is prohibited in Islam, any late payments by the export or import factors will be subject to a ‘late payment amount’ to be agreed on by the parties, not to ‘interest’.

- As trade of some goods and services are prohibited in Islam, the product or service related to the receivable must be approved by the other party before the first assignment by the export factor.

- Transactions with prohibition of assignment are not acceptable.

Since there is no reference to financing between the export and import factors in the GRIF, all the other terms and conditions of the GRIF are applicable in an Islamic International Factoring transaction in terms of a ‘wakalah/ tamleek’ (assignment). It should also be noted that there is no restriction in Islam to prevent trade between a Muslim and a non-Muslim. Therefore this new opportunity is open to all FCI members.

For more information and details regarding Islamic International factoring (publications of Yuce Uyanik – FCI legal committee), you may follow the link here

For specific inquiries or support for commencing Islamic International factoring you may contact your Regional Director or fci@fci.nl

Loading the documents, please wait a few seconds